Excise entries

This page provides information about:

- What to include in an excise entry

- Removal for home consumption

- Nil returns

What excise entries are

If you operate a Customs-controlled area (CCA), you must submit an excise entry to Customs. This is also called an excise lodgement or declaration. This will be submitted by a declarant acting on behalf of your organisation.

Excise entries are submitted through Trade Single Window (TSW) for each reporting period. This enables Customs to generate an invoice for the excise duty and any levies that may be payable.

Goods to include in excise entries

Your excise entry must include all excisable goods that were:

- physically removed for home consumption from the CCA during the reporting period

- used or consumed within the CCA during the reporting period, such as:

- product samples

- tastings

- goods used for sterilisation or cleaning

- within the CCA and destroyed, lost, or otherwise disposed of during the reporting period.

If no goods were removed during the reporting period, you must submit a nil return (an entry stating zero removals).

Alcoholic beverages with an alcohol content of 1.15% ABV or below

Alcoholic beverages with an alcohol content of 1.15% ABV or below made in the CCA are exempt from excise duty and do not need to be included in the excise entry. However, you must still keep business records of these products.

Removal for home consumption

“Removal for home consumption” (often referred to as “removal”) refers to goods that have been physically removed from your CCA or used within the CCA.

All goods that cross the boundary of your CCA are considered to be removed for home consumption unless the movement is:

- to another CCA under an authorisation or permit from Customs.

- temporary removal under section 235(1) of the Customs and Excise Act 2018.

- for export or moving goods to an export warehouse.

The legal definition of removal for home consumption is set out in Schedule 3, clause 3 of the Customs and Excise Act 2018.

Nil returns

You are required to lodge a nil return if either of the below apply:

- you are holding manufactured alcohol products and have not removed any from your Customs-controlled area (CCA) in your entry period

- removal of products from your CCA does not constitute being removed for home consumption.

The nil return is lodged in Trade Single Window (TSW) in the form of an excise entry. The return must be made within your entry period and in the way prescribed by the Customs (Nil Returns) Rules 2024 (PDF, 230 KB).

Failure to lodge a nil return is treated the same as failing to lodge a normal entry — penalties may apply.

Contact Customs if you are not using your CCA to manufacture or hold excisable goods for an extended time.

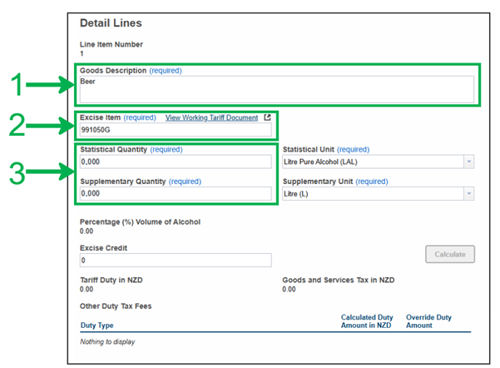

Nil returns are submitted through Trade Single Window (TSW) in the same way entries are normally submitted. Nil returns have the following differences to the entry details:

- In the description field, state the type of product you normally manufacture. If you normally make multiple products, select one.

- In the excise item number field, enter the excise item number for the product in the description field. Remove the periods from the item number.

- In the statistical quantity field, enter “0.000”. If supplementary quantity is required, enter “0.000” in the supplementary quantity field. 3 decimal places are required.

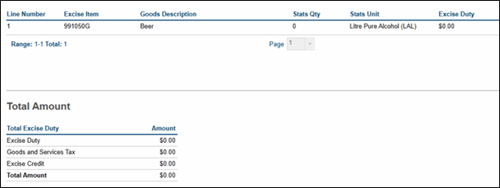

The entry summary will show there is no duty, GST, or levies to pay.

Excise entry offences

As an excise declarant, you must:

- submit accurate and complete excise entries

- notify Customs if there are any errors or omissions in your entries.

Otherwise, penalties may apply.